By

By

By Niall McCracken

WHILE the public focus of Northern Ireland’s spectacular property crash has been on homes and other properties repossessed and people made bankrupt, The Detail can reveal the existence of behind-the-scenes deals being reached with banks over distressed mortgages.

Banks here are actively negotiating shortfalls and writing down debts on private mortgages and at least three companies here now have units focused solely on achieving such settlements with lenders on behalf of clients.

However the deals are carried out in confidence between the lender and the borrower – or the borrower’s agent – and with no reference to the courts, meaning the scale and number of such deals is impossible to put a figure on.

Settlements are taking the forms of either a restructured repayment scheme – at a much lower rate than that which was written into the original mortgage plan – or the payment of a single lump sum which constitutes a full and final settlement, leaving the debtor with a clean credit rating.

Such settlements stem from the correct presentation to the financial institutions of a debtor’s position and can be settled for as little as 10 – 20% of the debt. The Detail is aware of one such deal where a shortfall of over £50,000 was settled for a single payment of £4,000.

But the banks themselves remain coy about the extent to which they engage in what could be termed “mortgage forgiveness” and, those who replied to our enquiries about such deals, did so only in the blandest terms.

However, Conor Devine who heads up the property team of Belfast based finance company GDP, says there has been a change of attitude in banks here over the past eighteen months that has gone largely unnoticed.

He says the practice known as ‘bank mediation’ has evolved into one of the largest parts of their business in Northern Ireland. It involves the company being employed by a borrower to act as the ‘mediator’ between them and the lending institution to try and find some middle ground in reaching a financial settlement.

Mr Devine says it is a simple idea that has produced effective results.

He said: “it doesn’t matter if you owe a bank a million pounds or a thousand pounds, if you don’t have the money you can’t pay, so that’s where you start from. Over the last year and a half it’s been our experience that banks have moved to a position in Northern Ireland where they admit there’s an issue and they’re happy to engage with the borrower.

“So we act for people who have borrowed money on assets who have found themselves in a situation where there is a huge difference between the current value of their assets and the value of debt that has built up.

“A simple way to look at it is if I owed you £100 but I can only afford to pay you £20, you are likely to say that you’re not interested. But after six months you might be interested in negotiating again and the banks are in the same space. “

The mortgage writedowns come as property repossessions are occurring at unprecedented rates here, with untold effects on the owners affected.

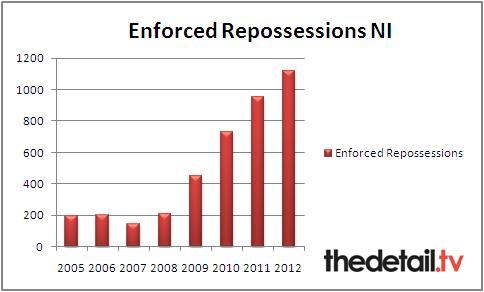

COURT REPOSSESSIONS

Figures provided by the Enforcement Judgements Office (EJO)

Official figures have continued to show an increase in the number of repossession cases going through the courts here.

The latest figures obtained by The Detail from the Enforcement Judgements Office (EJO) show that the number of evictions here peaked in 2012. See the bottom of the story for a detailed breakdown.

The EJO only becomes involved when there is a failure to deliver possession of a property following a final possession order. The office has statutory power to enforce the order.

Data from the Council of Mortgage Lenders (CML) released this month also indicates that Northern Ireland has the highest level of negative equity amongst the UK regions.

CML figures show that, of mortgages advanced in Northern Ireland since 2005, around 69,000 – some 35% – are in respect of properties now in negative equity – more than twice the level of the next most distressed region.

However, Mr Devine says the figures only serve to further illustrate how wide spread the problem is and might help explain why banks here have had to rethink their position.

He said: “You have to remember that banks have lent out money on mortgages worth one hundred grand or more, if the client goes bankrupt, that bank gets nothing, in that respect 10% of something is better than 90% of nothing.

“Our attitude is if a bank is not going to bankrupt you, why would you go bankrupt? There’s too many people would jump into bankruptcy too hastily.”

The Detail has spoken to another Belfast-based business which wishes to remain anonymous but has confirmed that it is also engaged in the area of bank mediation.

The Lord Chief Justice’s Office in Northern Ireland announced on 30 August 2011 that the ’Pre-Action Protocol for Possession Proceedings based on Mortgage Arrears in respect of Residential Property’ had been revised. The basic premise of the original protocol was to reduce repossession court proceedings through negotiation and exploring alternative ways of reaching a settlement.

The revised protocol set out the steps that lenders are expected to take before bringing a claim in the courts. It states that lenders should ensure that repossession action is a last resort and that lenders are expected to demonstrate that they have tried to discuss and agree alternatives to repossession with borrowers when they encounter difficulty with their mortgage repayments. The Protocol states:

“It is in the interests of the parties that mortgage payments or payments under home purchase plans are made promptly and that difficulties are resolved wherever possible without court proceedings. However in some cases an order for possession may be in the interest of both the lender and the borrower.”

For access to the full document click here.

We contacted a number of the main banks based in Northern Ireland for a statement on the matter: Bank of Ireland, Santander, First Trust, Danske and Ulster Bank.

First Trust confirmed that if a customer’s mortgage account falls into arrears it “actively engages with that customer and/or their appointed advisors to reach an agreed, sustainable solution.” It said it encouraged any customer facing financial difficulty to contact them at the “earliest opportunity” to work together to find the best way forward.

In a statement the Bank of Ireland said it was focused on “communicating with mortgage customers who may be experiencing current difficulties or who anticipate future difficulty in repaying their mortgage." It said its message to customers was to contact them.

However Danske Bank said that while it does “all it can” to help customers deal with financial difficulties it has “no plans to start negotiating shortfalls or writing down debts on private mortgages.”

We received no response from Ulster Bank or Santander.

AN AFFORDABILITY ISSUEIn a story by The Detail earlier this year we revealed that nearly three times as many property owners in Northern Ireland faced repossession through the courts than those in the Republic of Ireland between 2008 and 2011.

The figures reflected the experience of repossessions processed through courts and outlined profound differences in policy on both sides of the border: how banks in the south have been inclined to allow many mortgage cases to languish “unresolved” within the Irish justice system; and how the courts then deal with mortgage cases.

In January this year the Central Bank governor in the Republic of Ireland, Patrick Honohan, told an Oireachtas finance committee he wanted the banks to deal with mortgage arrears without resorting to personal insolvency legislation. He said banks needed to meet distressed customers and work out solutions on a case by case basis.

Mr Devine believes a similar attitude is being adopted in Northern Ireland. He says while it is a slow process, banks here are beginning to realise it’s not “unrealistic or unreasonable” for a borrower to try and restructure their loans. However, he maintains that transparency is key to making this process work.

He said: “We are only able to progress these cases to a situation where a deal can be done by providing the bank or lender with an assets and liability statement that will outline income and expenditure, basically providing full visibility of the financial capacity of the borrower.

“The bank would then digest this and once it understands the full financial situation of the borrower, a bit of realism comes into play and that’s when deals can be done. It doesn’t matter how much you owe a bank, it comes down to an affordability issue.”